Chandelier Exit ZLSMA StrategyIntroducing a Powerful Trading Indicator: Chandelier Exit with ZLSMA

If you're a trader, you know the importance of having the right tools and indicators to make informed decisions. That's why we're excited to introduce a powerful new trading indicator that combines the Chandelier Exit and ZLSMA: two widely-used and effective indicators for technical analysis.

The Chandelier Exit (CE) is a popular trailing stop-loss indicator developed by Chuck LeBeau. It's designed to follow the price trend of a security and provide an exit signal when the price crosses below the CE line. The CE line is based on the Average True Range (ATR), which is a measure of volatility. This means that the CE line adjusts to the volatility of the security, making it a reliable indicator for trailing stop-losses.

The ZLEMA (Zero Lag Exponential Moving Average) is a type of exponential moving average that's designed to reduce lag and improve signal accuracy. The ZLSMA takes into account not only the current price but also past prices, using a weighted formula to calculate the moving average. This makes it a smoother indicator than traditional moving averages, and less prone to giving false signals.

When combined, the CE and ZLSMA create a powerful indicator that can help traders identify trend changes and make more informed trading decisions. The CE provides the trailing stop-loss signal, while the ZLSMA provides a smoother trend line to help identify potential entry and exit points.

In our indicator, the CE and ZLSMA are plotted together on the chart, making it easy to see both the trailing stop-loss and the trend line at the same time. The CE line is displayed as a dotted line, while the ZLSMA line is displayed as a solid line.

Using this indicator, traders can set their stop-loss levels based on the CE line, while also using the ZLSMA line to identify potential entry and exit points. The combination of these two indicators can help traders reduce their risk and improve their trading performance.

In conclusion, the Chandelier Exit with ZLSMA is a powerful trading indicator that combines two effective technical analysis tools. By using this indicator, traders can identify trend changes, set stop-loss levels, and make more informed trading decisions. Try it out for yourself and see how it can improve your trading performance.

Warning: The results in the backtest are from a repainting strategy. Don't take them seriously. You need to do a dry live test in order to test it for its useability.

-

Here is a description of each input field in the provided source code:

length: An integer input used as the period for the ATR (Average True Range) calculation. Default value is 1.

mult: A float input used as a multiplier for the ATR value. Default value is 2.

showLabels: A boolean input that determines whether to display buy/sell labels on the chart. Default value is false.

isSignalLabelEnabled: A boolean input that determines whether to display signal labels on the chart. Default value is true.

useClose: A boolean input that determines whether to use the close price for extrema calculations. Default value is true.

zcolorchange: A boolean input that determines whether to enable rising/decreasing highlighting for the ZLSMA (Zero-Lag Exponential Moving Average) line. Default value is false.

zlsmaLength: An integer input used as the length for the ZLSMA calculation. Default value is 50.

offset: An integer input used as an offset for the ZLSMA calculation. Default value is 0.

-

Ty for checking this out and good luck on your trading journey! Likes and comments are appreciated. 👍

--

Credits to:

▪ @everget – Chandelier Exit (CE)

▪ @netweaver2022 – ZLSMA

Pesquisar nos scripts por "stop loss"

Reinforced RSI - The Quant Science This strategy was designed and written with the goal of showing and motivating the community how to integrate our 'Probabilities' module with their own script.

We have recreated one of the simplest strategies used by many traders. The strategy only trades long and uses the overbought and oversold levels on the RSI indicator.

We added stop losses and take profits to offer more dynamism to the strategy. Then the 'Probabilities' module was integrated to create a probabilistic reinforcement on each trade.

Specifically, each trade is executed, only if the past probabilities of making a profitable trade is greater than or equal to 51%. This greatly increased the performance of the strategy by avoiding possible bad trades.

The backtesting was calculated on the NASDAQ:TSLA , on 15 minutes timeframe.

The strategy works on Tesla using the following parameters:

1. Lenght: 13

2. Oversold: 40

3. Overbought: 70

4. Lookback: 50

5. Take profit: 3%

6. Stop loss: 3%

Time period: January 2021 to date.

Our Probabilities Module, used in the strategy example:

Simple SuperTrend Strategy for BTCUSD 4HHello guys!, If you are a swing trader and you are looking for a simple trend strategy, you should check this one. Based in the supertrend indicator, this strategy will help you to catch big movements in BTCUSD 4H and avoid losses as much as possible in consolidated situations of the market

This strategy was designed for BTCUSD in 4H timeframe

Backtesting context: 2020-01-02 to 2023-01-05 (The strategy has also worked in previous years)

Trade conditions:

Rules are actually simple, the most important thing is the risk and position management of this strategy

For long:

Once Supertrend changes from a downtrend to a uptrend, you enter into a long position. The stop loss will be defined by the atr stop loss

The first profit will be of 0.75 risk/reward ratio where half position will be closed. When this happens, you move the stop loss to break even.

Now, just will be there two situations:

Once Supertrend changes from a uptrend to a downtrend, you close the other half of the initial long position.

If price goes againts the position, the position will be closed due to breakeven.

For short:

Once Supertrend changes from a uptrend to a downtrend, you enter into a short position. The stop loss will be defined by the atr stop loss

The first profit will be of 0.75 risk/reward ratio where half position will be closed. When this happens, you move the stop loss to break even.

Like in the long position, just will be there two situations:

Once Supertrend changes from a downtrend to a uptrend, you close the other half of the initial short position.

If price goes againts the position, the position will be closed due to breakeven.

Risk management

For calculate the amount of the position you will use just a small percent of your initial capital for the strategy and you will use the atr stop loss for this.

Example: You have 1000 usd and you just want to risk 2,5% of your account, there is a long signal at price of 20,000 usd. The stop loss price from atr stop loss is 19,000. You calculate the distance in percent between 20,000 and 19,000. In this case, that distance would be of 5,0%. Then, you calculate your position by this way: (initial or current capital * risk per trade of your account) / (stop loss distance).

Using these values on the formula: (1000*2,5%)/(5,0%) = 500usd. It means, you have to use 500 usd for risking 2.5% of your account.

We will use this risk management for apply compound interest.

Script functions

Inside of settings, you will find some utilities for display atr stop loss, supertrend or positions.

You will find the settings for risk management at the end of the script if you want to change something. But rebember, do not change values from indicators, the idea is to not over optimize the strategy.

If you want to change the initial capital for backtest the strategy, go to properties, and also enter the commisions of your exchange and slippage for more realistic results.

Signals meanings:

L for long position. CL for close long position.

S for short position. CS for close short position.

Tp for take profit (it also appears when the position is closed due to stop loss, this due to the script uses two kind of positions)

Exit due to break even or due to stop loss

Some things to consider

USE UNDER YOUR OWN RISK. PAST RESULTS DO NOT REPRESENT THE FUTURE.

DEPENDING OF % ACCOUNT RISK PER TRADE, YOU COULD REQUIRE LEVERAGE FOR OPEN SOME POSITIONS, SO PLEASE, BE CAREFULL AND USE CORRECTLY THE RISK MANAGEMENT

The amount of trades closed in the backtest are not exactly the real ones. If you want to know the real ones, go to settings and change % of trade for first take profit to 100 for getting the real ones. In the backtest, the real amount of opened trades was of 194.

Indicators used:

Supertrend

Atr stop loss by garethyeo

This is the fist strategy that I publish in tradingview, I will be glad with you for any suggestion, support or advice for future scripts. Do not doubt in make any question you have and if you liked this content, leave a boost. I plan to bring more strategies and useful content for you!

Wunder Trend Reversal botWunder Trend Reversal bot

1. Wunder Trend Reversal Bot - this has only one goal to find a reversal of the trend.

2. The strategy determines, based on the specified value for the filter, a market reversal based on the price actions of the previous bars.

3. A short EMA is used to filter false signals after the reversal signal was received. Crossing the EMA and changing its direction confirms the trend change.

4. There are 2 ways to calculate stop loss and take profit. You can choose one of them:

- Classic stop loss and take profit in a fixed percentage

- ATR stop loss and take pro

5. ATR uses risk reward (R:R) to calculate take profit. The script calculates the risk-reward based on a certain stop loss level and uses it to calculate the take profit

6. A function for calculating risk on the portfolio (your deposit) has been added to the script. When this option is enabled, you get a calculation of the entry amount in dollars relative to your Stop Loss. In the settings, you can select the risk percentage on your portfolio. The loss will be calculated from the amount that will be displayed on the chart.

For example. Deposit - $1000, you set the risk to 1%. SL 5%. Entry volume will be $200. The loss at SL will be $10.10$ this is your 1% risk or 1% of the deposit.

Important! The risk per trade must be less than the Stop Loss value. If the risk is greater than SL, then you should use leverage.

The amount of funds entering the trade is calculated in dollars. This option was created if you want to send the dollar amount from Tradingview to the exchange. However, putting your volume in dollars you get the incorrect net profit and drawdown indication in the backtest results, as TradingView calculates the backtest volume in contracts.

To display the correct net profit and drawdown values in Tradingview Backtest results, use the ”Volume in contracts” option.

LuxAlgo - Backtester (S&O)The S&O Backtester is an innovative strategy script that encompasses features + optimization methods from our Signals & Overlays™ toolkit and combines them into one easy-to-use script for backtesting the most detailed trading strategies possible.

Our Signals & Overlays™ toolkit is notorious for its signal optimization methods such as the 'Optimal Sensitivity' displayed in its dashboard which provides optimization backtesting of the Sensitivity parameter for the Confirmation & Contrarian Signals.

This strategy script allows even more detailed & precise backtests than anything available previously in the Signals & Overlays™ toolkit; including External Source inputs allowing users to use any indicator including our other paid toolkits for take profit & stop loss customization to develop strategies, along with 10+ pre-built filters directly Signals & Overlays™' features.

🔶 Features

Full Sensitivity optimization within the dashboard to find the Best Win rates or Best Profits.

Counter Trade Mode to reverse signals in undesirable market conditions (may introduce higher drawdowns)

Built-in filters for Confirmation Signals w/ Indicator Overlays from Signals & Overlays™.

Built-in Confirmation exit points are available within the settings & on by default.

External Source Input to filter signals or set custom Take Profits & Stop Losses.

Optimization Matrix dashboard option showing all possible permutations of Sensitivity.

Option to Maximize for Winrate or Best Profit.

🔶 Settings

Sensitivity signal optimizations for the Confirmation Signals algorithm

Buy & Sell conditions filters with Indicator Overlays & External Source

Take Profit exit signals option

External Source for Take Profit & Stop Loss

Sensitivity ranges

Backtest window default at 2,000 bars

External source

Dashboard locations

🔶 Usage

Backtests are not necessarily indicative of future results, although a trader may want to use a strategy script to have a deeper understanding of how their strategy responds to varying market conditions, or to use as a tool for identifying possible flaws in a strategy that could potentially be indicative of good or bad performance in the future.

A strategy script can also be useful in terms of it's ability to generate more complete & configurable alerts, giving users the option to integrate with external processes.

In the chart below we are using default settings and built-in optimization parameters to generate the highest win rate.

Results like the above will vary & finding a strategy with a high win rate does not necessarily mean it will persist into the future, however, some indications of a well-optimized strategy are:

A high number of closed trades (100+) with a consistently green equity curve

An equity curve that outperforms buy & hold

A low % max drawdown compared to the Net Profit %.

Profit factor around 1.5 or above

In the chart below we are using the Trend Catcher feature from Signals & Overlays™ as a filter for standard Confirmation Signals + exits on a higher timeframe.

By filtering bullish signals only when the Trend Catcher is bullish, as well as bearish signals for when the Trend Catcher is bearish, we have a highly profitable strategy created directly from our flagship features.

While the Signals & Overlays features being used as built-in filters can generate interesting backtests, the provided External Sources can allow for even more creativity when creating strategies. This feature allows you to use many indicators from TradingView as filters or to trigger take-profit/stop-loss events, even if they aren't from LuxAlgo.

The chart below shows the HyperWave Oscillator from our Oscillator Matrix™ being used for take-profit exit conditions, exiting a long position on a profit when crossing 80, and exiting a short position when crossing 20.

🔶 Counter Trade Mode

Our thesis has always firmly remained to use Confirmation Signals within Signals & Overlays™ as a supportive tool to find trends & use as extra confirmation within strategies.

We included the counter-trade mode as a logical way to use the Confirmation signals as direct entries for longs & shorts within more contrarian trading strategies. Many traders can relate to using a trend-following indicator and having the market not respect its conditions for entries.

This mode directly benefits a trader who is aware that market conditions are generally not-so-perfect trends all the time. Acknowledging this, allows the user to use this to their advantage by introducing countertrend following conditions as direct entries, which tend to perform very well in ranging markets.

The big downfall of using counter-trade mode is the potential for very large max-drawdowns during trending market conditions. We suggest for making a strategy to consider introducing stop-loss conditions that can efficiently minimize max-drawdowns during the process of backtesting your creations.

Sensitivity Optimization

Within the Signals & Overlays™ toolkit, we allow users to adjust the Confirmation Signals with a Sensitivity parameter.

We believe the Sensitivity paramter is the most realistic way to generate the most actionable Confirmation Signals that can navigate various market conditions, and the Confirmation Signals algorithm was designed specifically with this in mind.

This script takes this parameter and backtests it internally to generate the most profitable value to display on the dashboard located in the top right of the chart, as well as an optimization table if users enable it to visualize it's backtesting.

In the image below, we can see the optimization table showing permutations of settings within the user-selected Sensitivity range.

The suggested best setting is given at the current time for the backtesting window that's customizable within the indicator. Optimized settings for technical indicators are not indicative of future results and the best settings are highly likely / guaranteed to change over time.

Optimizing signal settings has become a popular activity amongst technical analysts, however, the real-time beneficial applications of optimizing settings are limited & best described as complicated (even with forward testing).

🔶 Strategy Properties (Important)

We strongly recommend all users to ensure they adjust the Properties within the script settings to be in line with their accounts & trading platforms of choice to ensure results from strategies built are realistic.

🔶 How to access

You can see the Author's Instructions below to learn how to get access on our website.

The Flower - Multiple Strategy Options in OneStrategy Overview

This strategy code currently includes four separate strategies to be used to either aid in discretionary trading or to be used algorithmically through the third-party system Profitview (profitview.app). Support for Pineconnector for use with MetaTrader 4 is in the works. The strategies have been designed with cryptocurrency trading in mind, however, the fundamentals apply to other assets.

The four strategies currently included are labeled “TSI Cross” (the default setting), “Oscillator Bands”, “Scalping”, and “McG/MA Cross”. Detailed information for each independent strategy can be found below, including sample settings configurations for each. A dropdown menu to select the strategy can be found under the “Strategy Options” set of settings under the Input tab of the strategy settings menu.

Additionally, the option to receive only long or short signals can be found alongside the Strategy Choice menu.

Take profit, stop loss, and trailing percentages are also included, found at the bottom of the Input tab under “TT and TTP” as well as “Stop Loss”. Make sure to understand the TP/SL ratio that you desire before use, as the desired hit rate/profitability percentage will be affected accordingly.

The only visuals associated with the strategy are two McGinley Dynamic lines, red (slow length) and green (fast length). These are relevant to the McGinley Cross strategy, but can be used alongside the other strategies if desired.

When viewing the backtesting data in the TradingView Strategy Tester, ensure that “use bar magnifier” is activated. This option can be found in the Properties tab of the strategy settings menu.

Profitview Settings

If you wish to utilize Profitview’s automation system, find the included “Profitview Settings” under the Input tab of the strategy settings menu. If not, skip this section entirely as it can be left blank. Options will be “OPEN LONG TITLE”, “OPEN SHORT TITLE”, “CLOSE LONG TITLE”, and “CLOSE SHORT TITLE”. If you wished to trade SOL, for example, you would put “SOL LONG”, “SOL SHORT”, “SOL CLOSE LONG”, and “SOL CLOSE SHORT” in these areas. Within your Profitview extension, ensure that your Alerts all match these titles. A sample of our Profitview syntax can be found below.

To set an alert for use with Profitview, go to the “Alerts” tab in TradingView, then create an alert. Make sure that your desired asset and timeframe are currently displayed on your screen when creating the alert. Under the “Condition” option of the alert, select the strategy, then select the expiration time. If using TradingView Premium, this can be open-ended. Otherwise, select your desired expiration time and date. This can be updated whenever desired to ensure the strategy does not expire. Under “Alert actions”, nothing necessarily needs to be selected unless so desired. Leave the “Alert name” option empty. For the “Message”, delete the generated message and replace it with {{strategy.order.alert_message}} and nothing else.

Strategy Choices

As mentioned above, this strategy code contains four separate strategy options. A detailed breakdown of each follows below:

Total Strength Index (TSI) Cross

This strategy option is the default choice. The main signal involved in this strategy is a crossover or crossunder of the TSI value line and TSI signal line, however, there are a few other signals involved in the creation of a long or short entry. In addition to the TSI, the strategy includes an Average Directional Index (ADX) threshold value, Jurik Volatility Bands (JVB), a Stoch RSI threshold, and an oscillator of choice in conjunction with a threshold of 0. This oscillator choice can be selected under the “Signal Options” menu in the Input tab of the strategy settings. The default oscillator is the Detrended Price Oscillator (DPO), though the option for Chande Momentum (CMO) or Rate of Change (RoC) are both viable for this strategy.

Individual settings for these can be found in the Input tab under “Oscillator Settings” (TSI, Stoch RSI, DPO, CMO, ROC), “Band/Channel Settings” (Jurik Volatility Bands Length/Smoothing), and “Directional Settings” (ADX Smoothing Long, DI Length Short, ADX Threshold).

Sample settings for SOLUSDT using the 20M timeframe:

- Oscillator Settings -- DPO Length (21), DPO *not* centered, RSI (Stoch) Length (4), Stochastic Length (4), TSI Long Length (25), TSI Short Length (13), TSI Signal Length (13), K (3), D (3)

- Band/Channel Settings -- Jurik Volatility Bands Length (25), Jurik Volatility Bands Smoothing (5)

- Directional Settings – JVB Price Threshold (0), ADX Smoothing Long (5), DI Length Short (5), ADX Threshold (23)

- Take Profit/Stop Loss – 0.85% TP, 0.005% TTP, 1.3% SL

Oscillator Bands

This strategy involves the usage of bands or channels that use oscillators as a source input. The main signal for this strategy derives from a cross of the band or channel and a hline of 0. Additionally, this includes a “Directional Filter” and a “MA Filter”. The selections for all of these can be found in the “Signal Options” section of the Input tab.

First option is for Oscillator Choice and includes DPO, CMO, ROC, RSI, TSI, and the Jurik price line. The individual settings for these can be found in the “Oscillator Settings” section. Different channels can be selected for the upper or lower bands, though it is not necessary for them to differ. These current options include Bollinger Bands and Jurik Volatility Bands, the individual settings for each found in the “Band/Channel Settings” section. Next is the MA Filter, of which you can select SMA, EMA, SMMA, WMA, VWMA, KAMA, JMA, or McGinley Dynamic. All options for these settings can be found in the “MA Filter Settings” section. Lastly, the Directional Filters can be selected for either direction like the upper/lower band selection. These filters include the ADX, Bull-Bear Power (BBP), Parabolic SAR (PSAR), or Jurik.

Sample settings for WAVESUSDT using the 20M timeframe:

- Oscillator Choice – DPO (Length – 30, uncentered)

- Upper and Lower Band – JVB Upper/Lower (Jurik Volatility Bands Length – 25; Smoothing – 10)

- MA Filter – VWMA – (MA Length – 40; Source – Open)

- Directional Filter – ADX (ADX Smoothing Long – 14; DI Length Short – 5; ADX Threshold – 22)

- Take Profit/Stop Loss – 0.85% TP, 0.005% TTP, 1.3% SL

Scalping

This strategy heavily relies on the usage of Parabolic SAR, accompanied by a “Directional Filter” (as discussed in the previous section) other than PSAR. This strategy can provide a higher frequency of trades as opposed to the other strategies available, however, it comes with slightly higher risk inherently. A riskier take profit/stop loss spread is recommended here, though risk should always be managed. The settings required for this strategy are all found under the “Directional Settings” section of the strategy inputs.

Sample settings for NEARUSDT using the 20M timeframe:

- Directional Filter set to ADX

- Directional Settings – ADX Smoothing Long (5), DI Length Short (5), ADX Threshold (22), PSAR Start Value (0.02), PSAR Increment (0.005), PSAR Max Value (0.15), PSAR Source (Close)

- Take Profit/Stop Loss – 0.75% TP, 0.005% TTP, 1.5% SL

McGinley Cross

This strategy revolves around the crossing of two McGinley Dynamic lines of varying lengths alongside an ADX filter as well as a DPO filter. McGinley is used as opposed to a standard moving average cross strategy as it adjusts for shifts in market speed and can better gauge market trends. The McGinley length settings can be found with the “MA Filter” settings, labeled as Fast Length and Slow Length. The fast length number should be smaller than the slow length.

Sample settings for SOLUSDT using the 20M timeframe:

- Oscillator Settings – DPO Length (30), uncentered

- MA Filter Settings – McGinley Fast Length (4), McGinley Slow Length (21)

- Take Profit/Stop Loss – 0.85% TP, 0.005% TTP, 1.4% SL

Comprehensive Settings List

Date and Time: From date and to date, adjustable for backtesting purposes.

Signal Options:

Oscillator Choices: Chande Momentum Oscillator (CMO), Detrended Price Oscillator (DPO), Rate of Change (ROC), Relative Strength Index (RSI), True Strength Index (TSI), Jurik Volatility Bands Priceline (JVB) – *** for use with TSI Cross or Oscillator Bands strategies only ***

Upper and Lower Band/Channel Choices: Bollinger Bands (BB) or Jurik Volatility Bands (JVB) -- *** for use with Oscillator Bands strategy only ***

MA/McG Filter: SMA, EMA, RMA, WMA, VWMA, Kaufmann MA, Jurik MA, McGinley Dynamic -- *** for use with Oscillator Bands strategy only ***

Directional Filter Long/Short: Average Directional Index (ADX), Bull/Bear Power (BBP), Parabolic SAR (PSAR), Jurik -- *** for use with Oscillator Bands strategy only ***

Profitview Settings: *** For use with ProfitView extension only, otherwise ignore ***

Oscillator Settings: *** For use with TSI Cross, Oscillator Bands, and McGinley Cross strategies ***

CMO Length, CMO Source – for Chande Momentum Oscillator

DPO Length, DPO Centered – for Detrended Price Oscillator

RoC Length, RoC Source – for Rate of Change

RSI Length, RSI MA Length – for Relative Strength Index

RSI (Stoch) Length, Stochastic Length, Stoch RSI Source, K, D – for Stochastic RSI

TSI Long Length, TSI Short Length, TSI Signal Length – for True Strength Index

Band/Channel Settings: *** For use with Oscillator Bands strategy ***

Jurik Volatility Bands Length, Jurik Volatility Bands Smoothing – for Jurik Volatility Bands

Bollinger Band Length, Bollinger Band Multiplier – for Bollinger Bands

Directional Settings: *** For use with Scalping and Oscillator Bands strategies ***

JVB Price Threshold – for Jurik Volatility as a directional setting

ADX Smoothing Long, DI Length Short, ADX Threshold – for Average Directional Index

PSAR Start Value, PSAR Increment, PSAR Max Value, PSAR Source – for Parabolic SAR

MA Filter Settings: *** For use with Oscillator Bands and McGinley Cross strategies ***

McGinley Fast/Slow Length – for McGinley Dynamic

MA Length, MA Source, MA Offset – for any other moving average

TP and TTP / Stop Loss: *** For use with ALL strategies ***

Long/Short Take Profit % -- for standard take profit settings

Enable Trailing, Trailing Take Profit % -- for trailing settings

Stop Loss % -- for standard stop loss settings; trailing can be enabled or disabled for stop loss

Disclaimers:

Some open-source code has been included -- Jurik Volatility Bands (by "ProValueTrader") and Trailing Take Profit/Stop Loss code (by jason5480). Additional code was used from the TradingView built-ins.

These strategies do NOT guarantee future returns. Apply caution in trading regardless of discretionary or algorithmic. Understand the concepts of risk/reward and the intricacies of each strategy choice before utilizing them in your personal trading.

Invites to the strategy will only be disseminated to those with express consent and knowledge of the invite prior to the action itself.

Wunder Keltner botWunder Keltner bot

1. Wunder Keltner bot is based on the breakout of the Keltner channel. For calculation, 2 channels are used, one for long trades, and the other for short trades. The division into 2 channels is used for more accurate entry calculations depending on trend directions.

2. The ADX indicator is used to filter signals and determine the trend strength. ADX determines the strength of the trend and confirms the entry into the strategy if the value is greater than the level indicated in the settings.

3. There are 3 ways to calculate Stop Loss and Take Profit. You can choose one of them:

Classic Stop Loss and Take Profit in a fixed percentage

ATR Stop Loss

Keltner. Stop Loss, which is set on the opposite Keltner’s Channel Band from Keltner breakout.

4. ATR and Keltner use Risk Reward (R:R) to calculate Take Profit. The script calculates Risk Reward based on the determined Stop loss level and uses the ration to calculate Take Profit.

5. A function for calculating risk on the portfolio (your deposit) has been added to the script. When this option is enabled, you get a calculation of the entry amount in dollars relative to your Stop Loss. In the settings, you can select the risk percentage on your portfolio. The loss will be calculated from the amount that will be displayed on the chart.

For example. Deposit - $1000, you set the risk to 1%. SL 5%. Entry volume will be $200. The loss at SL will be $10.10$ this is your 1% risk or 1% of the deposit.

Important! The risk per trade must be less than the Stop Loss value. If the risk is greater than SL, then you should use leverage.

The amount of funds entering the trade is calculated in dollars. This option was created if you want to send the dollar amount from Tradingview to the exchange. However, putting your volume in dollars you get the incorrect net profit and drawdown indication in the backtest results, as TradingView calculates the backtest volume in contracts.

To display the correct net profit and drawdown values in Tradingview Backtest results, use the ”Volume in contract” option.

MACD MTF Strategy [JoseMetal]============

ENGLISH

============

- Description:

This strategy uses my indicator MACD MTF (check my profile) to generate entries, it also has ATR to define Stop Loss and Take Profit if needed.

The strategy has several customizable options, which allows you to refine the strategy for your asset and timeframe.

You can customize settings for ALL indicator settings (MACD MTF and ATR).

- CUSTOM CONDITIONS TO ENTER A POSITION:

1. Both MACDs agree (current timeframe and higher timeframe).

2. Current timeframe MACD crossover.

3. Higher timeframe MACD crossover.

4. MACDs no longer agree with each other.

- EXIT CONDITION:

1. Predefined Stop Loss and Take Profit based on ATR (stop can be previous wick).

2. MACDs no longer agree with each other.

3. Opposite position entry.

- STOP LOSS TYPE:

1. ATR.

2. Previous wick.

- OTHER OPTIONS:

You can customize any setting for my MACD MTF and ATR.

- Visual:

ATR is shown for the Stop Loss / Take Profit.

The script prints the Take Profit as a green line, Stop Loss as a red line and entry price with a white line.

- Recommendations:

Recommended on 8H or 12H timeframe for the CURRENT timeframe, while using DAILY for the higher timeframe on the MACD MFT (by default).

Entry when BOTH MACDs agree and exit on opposite entry, this has NO TAKE PROFIT or STOP LOSS, so be careful, but gives the BEST profit overall, and being on 8H/12H + Daily lets you relax.

- Customization:

As you can see, almost everything is customizable, for colors and plotting styles check the "Style" tab.

Enjoy!

============

ESPAÑOL

============

- Descripción:

Esta estrategia utiliza mi indicador MACD MTF (revisa mi perfil) para generar entradas, también cuenta con ATR para definir Stop Loss y Take Profit si es necesario.

La estrategia tiene varias opciones personalizables, lo te le permiten refinar la estrategia para te activo y temporalidad.

Puedes personalizar la configuración de TODOS los indicadores (MACD MTF y ATR).

- CONDICIONES PERSONALIZADAS PARA ENTRAR EN UNA POSICIÓN:

1. Ambos MACDs coinciden (temporalidad actual y temporalidad superior).

2. Cruce del MACD en el marco de tiempo actual.

3. Cruce del MACD en el marco temporal superior.

4. Los MACD ya no coinciden entre sí (están en desacuerdo).

- CONDICIÓN DE SALIDA:

1. Stop Loss y Take Profit predefinidos basados en el ATR (el stop puede ser la mecha anterior).

2. Los MACDs ya no coinciden entre sí (están en desacuerdo).

3. Entrada en posición contraria.

- TIPO DE STOP LOSS:

1. ATR.

2. Mecha anterior.

- OTRAS OPCIONES:

Puede personalizar cualquier ajuste para mi MACD MTF y ATR.

- Visual:

El ATR se muestra para el Stop Loss / Take Profit.

El script imprime el Take Profit como una línea verde, el Stop Loss como una línea roja y el precio de entrada con una línea blanca.

- Recomendaciones:

Se recomienda en el marco de tiempo 8H o 12H para el marco de tiempo ACTUAL, mientras que se utiliza DIARIO para el marco de tiempo superior en el MACD MFT (por defecto).

Entrar cuando AMBOS MACDs están de acuerdo y salir en la entrada opuesta, esto no tiene TAKE PROFIT o STOP LOSS, así que tenga cuidado, pero da el MEJOR beneficio en general, y estar en 8H/12H + Diario le permite relajarse.

- Personalización:

Como puedes ver, casi todo es personalizable, para colores y estilos de trazado revisa la pestaña "Estilo".

¡Que lo disfrutes!

SuperTrend Multi Time Frame Long and Short Trading Strategy

Hello All

This is non-repainting Supertrend Multi Time Frame script, I got so many request on Supertrend with Multi Time Frame. This is for all of them ..I am making it open for all so you can change its coding according to your need.

How the Basic Indicator works

SuperTrend is one of the most common ATR based trailing stop indicators.

In this version you can change the ATR calculation method from the settings. Default method is RMA.

The indicator is easy to use and gives an accurate reading about an ongoing trend. It is constructed with two parameters, namely period and multiplier. The default values used while constructing a Supertrend indicator are 10 for average true range or trading period and three for its multiplier.

The average true range (ATR) plays an important role in 'Supertrend' as the indicator uses ATR to calculate its value. The ATR indicator signals the degree of price volatility .

The buy and sell signals are generated when the indicator starts plotting either on top of the closing price or below the closing price. A buy signal is generated when the ‘Supertrend’ closes above the price and a sell signal is generated when it closes below the closing price.

It also suggests that the trend is shifting from descending mode to ascending mode. Contrary to this, when a ‘Supertrend’ closes above the price, it generates a sell signal as the colour of the indicator changes into red.

A ‘Supertrend’ indicator can be used on spot, futures, options or forex, or even crypto markets and also on daily, weekly and hourly charts as well, but generally, it fails in a sideways-moving market.

How the Strategy works

This is developed based on SuperTrend.

Use two time frame for confirm all entry signals.

Two time frame SuperTrend works as Trailing stop for both long and short positions.

More securely execute orders, because it is wait until confine two time frames(example : daily and 30min)

Each time frame developed as customisable for user to any timeframe.

User can choose trading position side from Long, Short, and Both.

Custom Stop Loss level, user can enter Stop Loss percentage based on timeframe using.

Multiple Take Profit levels with customisable TP price percentage and position size.

Back-testing with custom time frame.

This strategy is develop for specially for automation purpose.

The strategy includes:

Entry for Long and Short.

Take Profit.

Stop Loss.

Trailing Stop Loss.

Position Size.

Exit Signal.

Risk Management Feature.

Backtesting.

Trading Alerts.

Use the strategy with alerts

This strategy is alert-ready. All you have to do is:

Go on a pair you would like to trade

Create an alert

Select the strategy as a Trigger

Wait for new orders to be sent to you

This is develop for specially for automating trading on any exchange, if you need to get that automating service for this strategy or any Tradingview strategy or indicator please contact me I am have 8 year experience on that field.

I hope you enjoy it!

Thanks,

Ranga

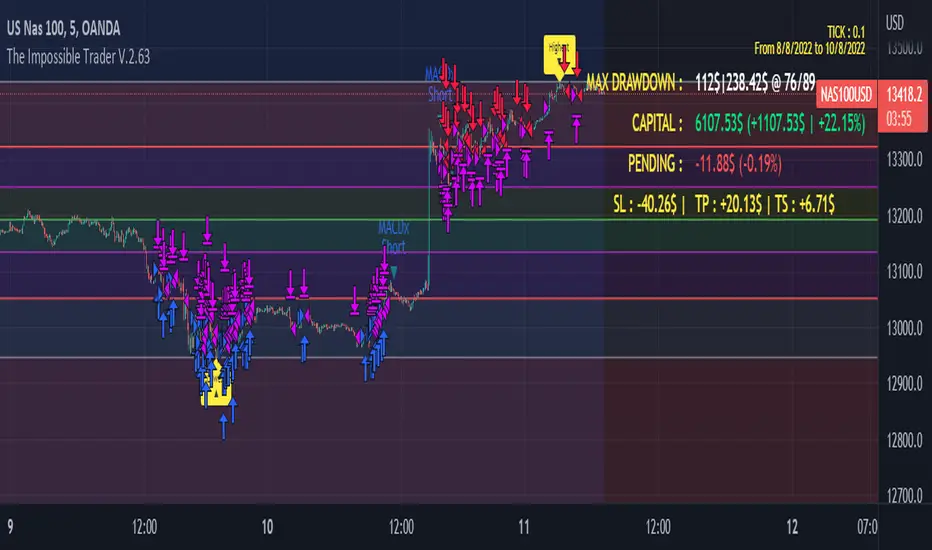

The Impossible TraderTHE IMPOSSIBLE TRADER

A simple, but effective High Freq Strategy script based on MACD or RSI trend, with extra customizable Alert Messages for Bots.

WHAT IT DOES

This script (works best at lower TimeFrames) just follow the trend of MACD or RSI on your asset.

Why it should work? Because in an upper trend, there are more chance of green candles than reds. And in dump trend there are more chance of red candles than greens.

While trend is positive, it will try to open Long orders as fast as possible at market price.

While trend is negative, it will try to open Short orders as fast as possible at market price.

HOW TO SETUP YOUR PREFERENCES

Capital : Insert a % of Margin you want to use for your positions (usually 30% is quite good)

Leverage : Choose leverage based on your plans

Trail Tick @ : This value (in Tick) tell the script "when" the "Trail Stop" order must be activated (from the Entry price)

Offset Tick @ : This is the price (in Tick) from the Trail Stop Price activated. Basically it is a Stop Loss that follow the price at a fixed distance.

SL Tick @ : Set a Stop Loss at amount Tick distance from the Entry Price. (Let's call it a Safety Stop Loss for bad decisions...)

TP Tick @ : Set a Take Profit at amount Tick distance from the Entry Price. Sometimes is better to exit in full Gain than keep positions.

Strategy : You can choose a Only Long, Only Short or Long+Short sametime strategy.

with MACD or RSI : You can try the strategy applied on MACD or applied on customizable RSI EMA

EMA : If you choosed RSI EMA, you can set any value for your testing (usually 80-120 works very nice)

Exit order after bars : Some Exchanges / Brokers apply fixed cost, and a strategy too fast could not be productive. This set will let you to delay the Exit Order on already Opened positions.

Keep Stop Loss active : If you are planning a delay for Exit Orders, sometime could be useful to keep activated Stop Loss.

Strategy Preset : Some preset I've found interesting, with good results.

BackTest Days : If there are too many results and script doesn't work, you can choose a closer range to show results.

EXTRA FEATURES

On Screen Display : OSD will show you some realtime stats about your strategy, like Asset Tick, Trading Period Range, Drawdown, Gains and not closed trade.

Alert Message : You can enter custom Long Entry/Exit and Short Entry/Exit message for your Bots (like AutoView, WunderBit, etc...). When alert is triggered, you can send custom message with {{strategy.order.comment}} in the text field

AutoView Alert Message : If you are user of AutoView, you can generate your calls. Those are tested only on Oanda with index like Sp500, US100, Us30.

TIPS ON USE

Some asset on TradingView require an higher initial capital. Go to this Script Settings -> Properties and rise Initial Capital.

Be aware of commissions and spread when evalutating a strategy. Go to this Script Settings -> Properties and set Commission and Slippage

Trail Stop and Ticks could be difficult to understand, but very profitable. Please take your time and study how it works.

Consider Tick like the minimum movement your asset can do. Ticks occurs "intra-bar", so some of your positions could be closed almost instantly.

Consider Trail Stop like a Stop Loss that keep always the same distance from your positions, but never came back . If you are in gain, say of 10 Ticks, and your Trail have 5 Ticks, this means for sure a close at minimum 5 Ticks from Entry Price.

On Screen Display will show you Ticks for your asset. This will help you on strategy settings, because not all asset responds on the same way.

ONLY LONG EXAMPLE

ONLY SHORT EXAMPLE

Double SupertrendThis strategy is based on a custom indicator that was created based on the Supertrend indicator. At its core, there are always 2 super trend indicators with different factors to reduce market noise (false signals).

The strategy/indicator has some parameters to improve the signals and filters.

TECHNICAL ANALYSIS

☑ Show Indicators

This option will enable/disable the Supertrend indicators on the chart.

☑ Length

The length will be used on the Supertrend Indicator to calculate its values.

☑ Dev Fast

The fast deviation or factor from one of the super trend indicators. This will be the leading indicator for entry signals, as well as for the exit signals.

☑ Dev Slow

The slow deviation or factor from one of the super trend indicators. This will be the confirmation indicator for entry and exit signals.

☑ Exit Type

It's possible to select from 4 options for the exit signals. Exit signals always take profit target.

☑ ⥹ Reversals

This option will make the strategy/indicator calculate the exit signals based on the difference between the given period's highest and lowest candle value (see Period on this list). It's displayed on the chart with the cross. As it's possible to verify in the image below, there are multiple exit spots for every entry.

☑ ⥹ ATR

Using ATR as a base indicator for exit signals will make the strategy/indicator place limit/stop orders. Candle High + ATR for longs, Candle Low - ATR for shorts. The strategy will show the ATR level for take profit and stick with it until the next signal. This way, the take profit value remains based on the candle of the entry signal.

☑ ⥹ Fast Supertrend

With this option selected, the exit signals will be based on the Fast Supertsignal value, mirrored to make a profit.

☑ ⥹ Slow Supertrend

With this option selected, the exit signals will be based on the Slow Supertsignal value, which is mirrored to take profit.

☑ Period

This will represent the number of candles used on the exit signals when Reversals is selected as Exit Type. It's also used to calculate the gradient used on the Fills and Supertrend signals.

☑ Multiplier

It's used on the take profit when the ATR option is selected on the Exit Type.

STRATEGY

☑ Use The Strategy

This will enable/disable the strategy to show the trades calculations.

☑ Show Use Long/Short Entries

Option to make the strategy show/use Long or Short signals. Available only if Use The Strategy is enabled

☑ Show Use Exit Long/Short

Option to make the strategy show/use Exit Long or Short signals (valid when Reversals option is selected on the Exit Type). Available only if Use The Strategy is enabled

☑ Show Use Add Long/Short

Option to make the strategy show/use Add Long or Short signals. With this option enabled, the strategy will place multiple trades in the same direction, almost the same concept as a pyramiding parameter. It's based on the Fast Supersignal when the candle fails to cross and reverses. Available only if Use The Strategy is enabled

☑ Trades Date Start/End

The date range that the strategy will check the market data and make the trades

HOW TO USE

It's very straightforward. A long signal will appear as a green arrow with a text Long below it. A short signal will appear as a red arrow with a text Short above it. It's ideal to wait for the candle to finish to validate the signal.

The exit signals are optional but give a good idea of the configuration used when backtesting. Each market and timeframe will have its own configuration for the best results. On average, sticking to ATR as an exit signal will have less risk than the other options.

☑ Entry Signals

Follow the arrows with Long/Short texts on them. Wait for the signal candle to close to validate the entry.

☑ Exit Signals

Use them to close your position or to trail stop your orders and maximize profits. Select the exit type suitable for each timeframe and market

☑ Add Entries

It's possible to increase the position following the add margin/contracts based on the Add signals. Not mandatory, but may work as reentries or late entries using the same signal.

☑ What about Stop Loss?

The stop-loss levels were not included as a separated signal because it's already in the chart. There are some possible ideas for the stop loss:

☑⥹ Candle High/Low (2nd recommend option)

When it's a Long signal from the entry signal candle, the stop loss can be the Low value of the same candle. Very tight stop loss in some cases, depending on the candle range

☑⥹ Local Top/Bottom

Selecting the local top/bottom as stop loss will give the strategy more room for false breakouts or reversals, keeping the trade open and minimizing noises. Increases the risk

☑⥹ Fast Supertrend (1st recommend option)

The fast supertrend can be used as stop-loss as well. making it a moving level and working close to trail stop management

☑⥹ Fixed Percentage

It's possible to use a fixed risk percentage for the trades, making the risk easier to control and project. Since the market volatility is not fixed, this may affect the accuracy of the trades

☑⥹ Based on the ATR (3rd recommend option)

When the exit type option ATR is selected, it will display the take profit level for that entry. Just mirror that value and put it as stop-loss, or multiply that amount by 1.5 to have more room for market noise.

EXAMPLE CONFIGURATIONS

Here are some configuration ideas for some markets (all of them are from crypto, especially futures markets)

BTCUSDT 15min - Default configuration

BTCUSDT 1h - Length 10 | Dev Fast 3 | Dev Slow 4 | Exit Type ATR | Period 50 | Multiplier 1

BTCUSDT 4h - Length 10 | Dev Fast 2 | Dev Slow 4 | Exit Type ATR | Period 50 | Multiplier 1

ETHUSDT 15min - Length 20 | Dev Fast 1 | Dev Slow 3 | Exit Type Fast Supertrend | Period 50 | Multiplier 1

IOTAUSDT 15min - Length 10 | Dev Fast 1 | Dev Slow 2 | Exit Type Slow Supertrend | Period 50 | Multiplier 1

OMGUSDT 15min - Length 10 | Dev Fast 1 | Dev Slow 4 | Exit Type Slow Supertrend | Period 50 | Multiplier 1

VETUSDT 15min - Length 10 | Dev Fast 3 | Dev Slow 4 | Exit Type Slow Supertrend | Period 50 | Multiplier 1

HOW TO FIND OTHER CONFIGURATIONS

Here are some steps to find suitable configurations

select a market and time frame

enable the Use This Strategy option on the strategy

open the strategy tester panel and select the performance summary

open the strategy configuration and go to properties

change the balance to the same price of the symbol (example: BTCUSDT 60.000, use 60.000 as balance)

go back to the inputs tab and keep changing the parameters until you see the net profit be positive and bigger than the absolute value of the drawdown

in case you can't find a suitable configuration, try other timeframes

Since the tester reflects what happened in the past candles, it's not guaranteed to give the same results. However, this indicator/Strategy can be used with other indicators as a leading signal or confirmation signal.

RSI Strategy w/ Trailing SL / TP Optimized for Crypto [Strategy]This strategy is designed to use the RSI and EMA filters. A 200 period EMA is used for short / long filters, and the 50 period EMA is used to determine the direction of the short term trend.

In addition, the script uses "rate of change" for the fast EMA (trend), volume , RSI (momentum), and price (volatility) and only takes trades when all are in optimal conditions.

I.E., the EMA is in an uptrend, the volume is increasing, price is in an uptrend, and the RSI is in an uptrend, so we will place a Long trade.

This strategy uses EMAs as a trailing stop loss and take profit. As this is a trend following strategy, the idea is to maximize profits when correct and minimize losses when

wrong.

It was designed specifically using crypto pairs, and was optimized for the 10 minute chart.

My goal was to get the best use out of the RSI indicator. I was originally an MACD fanboy, but have recently converted.

Want to help me improve this code or strategy? Have suggestions for improvement? Leave them in the comments below.

Thanks for using my script! I hope it works well for you and good luck in the markets.

If you have any questions, please leave them in the comments and I'll do my best to respond.

This script does not repaint as it only relies on close data to make a decision to enter a trade.

How to use this strategy:

___________________________

Enable Long Entries? - Used to enable or disable the strategy from executing long entries.

Enable Short Entries? - Used to enable or disable the strategy from executing short entries.

How Many Bars To Look Back for Hi/Lo: - This is used for the Stop Loss and Take Profit targets. An integer of bars is used to look back and calculate the values.

RSI Length (Rec: 8) - The length of the RSI

Source - The RSI Source

Use Slow EMA? - If checked, a 200 period EMA will be used to filter entries long or short (only take shorts when the price is below, long when above). In addition, the script will close any trades that cross the 200 period EMA. By default this is disabled.

EMA Slow - the period of the Slow EMA (200 by default)

EMA Slow Src - what to use to calculate the Slow EMA (high by default)

EMA Fast - The Fast EMA (50 period) is used to calculate the direction of the short term trend. This also factored into the Rates of Change.

EMA Fast Src - what to use to calculate the Fast EMA

ATR Length - If used, the ATR length is used to calculate the Stop Loss and Take Profit targets.

SL Multiplier - The distance away from the initial value to multiply the Stop Loss

TP Multiplier - The distance away from the initial value to multiply the Take Profit.

Use EMA as SL / TP? - If true (default) a 3 period EMA is used to calculate Stop Loss and Take Profit targets. Else, an ATR is used to calculate these values.

Stop Loss / Take Profit Offset - Default: 3 - this is used to shift the EMA / ATR Stop Loss and Take Profit lines to the right X bars. This is to ensure that they are hit properly and not exceeded.

Short Len Vol - Use to calculate the volume of the short length, used in rate of change calculations

Long Len - Use to calculate the volume of the long length, used in rate of change calculations

RSI Long Entry Val - Minimum RSI crossover value to enter a trade Long. If the RSI is below this value, trade entries are not valid.

RSI Long Cutoff Threshold - Long entry RSI value cutoff to no longer enter trades. If the RSI is above this value, trades entries are not valid.

RSI Short Entry Val - Minimum RSI crossover value to enter a trade Short. If the RSI is above this value, trade entries are not valid.

RSI Short Cutoff Threshold - Short entry RSI value cutoff to no longer enter trades. If the RSI is below this value, trades entries are not valid.

ROC Fast EMA - Calculates the rate of change between the Fast Ema now and 'X' bars ago. \n\n For a long entry, a positive value is needed, and for a short entry, a negative value is needed.

ROC Price - Calculates the rate of change between the most recent price close and 'X' bars ago. \n\n For a long entry, a positive value is needed, and for a short entry, a negative value is needed.

ROC RSI - Calculates the rate of change between the RSI now and 'X' bars ago. \n\n For a long entry, a positive value is needed, and for a short entry, a negative value is needed.

Use Close for SL - Default = Off - If checked, when a candle hits the stop loss, the trade will close on the next candle. If unchecked, the trade will remain open until the candle closes at or beyond the stop loss lines.

Custom Message Boxes - Primarily used for bots, but can be used to also insert your own messages for your trading alerts.

BTC|scanner|LONG|SHORT|30min STRATEGY- This strategy based on BTC|Scanner| v0.6b INDICATOR.

- Stop loss and take profit settings are available.

- This strategy can be used on a 30m timeframe and does not require fine tuning.

Detailed description of the strategy:

-According to the terms of the strategy:

-The initial deposit is $ 1000.

-The entry into the trade is carried out with the leverage from x3 to x8.

-Each entry/exit is shown by up/down arrows on the chart, the number of arrows shows the size of the leverage in the trade.

-Enter the trade with 100% of the deposit.

-All of the above suggests that with the input signal and the indication of the three arrows, an entry in the amount of$3000 will be made. If the shooter is 5, then$5000.

-Exit from the long/short position under the strategy conditions is carried out by 33% of the initial position volume on all TP (you can specify an unrealistic value of TP3, then the exit of 33% will be due only to an increase in the risk of further holding the position, but this can both increase profit and reduce it).

-To avoid distortion of the strategy indicators due to compound interest, it is recommended to take a period of a month to view statistics.

-The "Enter Confirm" field displays the confirmation of the trade, if several signals appear sequentially, the trade will be executed, and if the signal appears once, the trade will be skipped.

-The "ratio" field indicates the coefficient of change in activity on the current bar from the previous bar.

-The "Corner" field changes the angle of the stop loss correction depending on the time in the direction of reducing the loss.

-The "Short trigger" field indicates from which phase of activity you can open a short trade, conditionally this is a sinusoid with a lower limit of 0 and an upper limit of 100, but the sinusoid itself does not necessarily reach 0 and 100, the activity can stop at 80 and go towards 0 (initially the value 65 is specified).

-The "TP and Stop loss" fields are the percentage of profit / loss multiplied by 10. (the value 35 corresponds to 3.5%, 20-2% , and so on).

-The "cross action" field includes closing the trade when the activity sinusoid reaches the value of 99, regardless of any other calculations.

-The stop loss is displayed on the chart with orange and white dots.

The indicator and strategy can be applied not only to BTC , but it often has poor statistics on illiquid instruments.

////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////

- Эта стратегия основана на индикаторе BTC|Scanner| v0.6b.

- Доступны настройки стоп-лосса и тейк-профита.

- Эта стратегия может быть использована на 30-минутном таймфрейме и не требует тонкой настройки.

Подробное описание стратегии:

-Начальный депозит составляет 1000 долларов.

-Вход в сделку осуществляется с кредитным плечом от х3 до х8.

-Каждый вход/выход отображается стрелками вверх/вниз на графике, количество стрелок показывает размер кредитного плеча в сделке.

-Вход в сделку на 100% депозита.

-Все вышесказанное говорит о том, что с помощью входного сигнала и индикации трех стрелок будет совершен вход на сумму 3000 долларов. Если стрелок 5, то 5000 долларов.

-Выход из длинной/короткой позиции по условиям стратегии осуществляется на 33% от объема начальной позиции по всем ТП (можно указать нереальное значение ТП3, тогда выход на 33% будет обусловлен только увеличением риска дальнейшего удержания позиции, но это может как увеличить прибыль, так и уменьшить ее).

-Чтобы избежать искажения показателей стратегии из-за сложных процентов, рекомендуется использовать месячный период для просмотра статистики.

-В поле "Enter Confirm" отображается подтверждение сделки, если последовательно появится несколько сигналов, сделка будет выполнена, а если сигнал появится один раз, сделка будет пропущена.

-Поле "ratio" указывает коэффициент изменения активности на текущем баре по сравнению с предыдущим баром.

-Поле "Corner" изменяет угол коррекции стоп-лосса в зависимости от времени в направлении уменьшения убытка.

-Поле "Short trigger" указывает, с какой фазы активности вы можете открыть короткую сделку, условно это синусоида с нижней границей 0 и верхней границей 100, но сама синусоида не обязательно достигает 0 и 100, активность может остановиться на 80 и пойти в сторону 0 (изначально указано значение 65).

-Поля "TP и Stop loss" - это процент прибыли / убытка, умноженный на 10. (значение 35 соответствует 3,5%, 20-2% и так далее).

-Поле "cross action" включает закрытие сделки, когда синусоида активности достигает значения 99, независимо от любых других расчетов.

-Стоп-лосс отображается на графике оранжевыми и белыми точками.

Индикатор и стратегию можно применить не только к BTC , но зачастую он имеет плохую статистику на неликвидных инструментах.

////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////

888 BOT #backtest█ 888 BOT #backtest (open source)

This is an Expert Advisor 'EA' or Automated trading script for ‘longs’ and ‘shorts’, which uses only a Take Profit or, in the worst case, a Stop Loss to close the trade.

It's a much improved version of the previous ‘Repanocha’. It doesn`t use 'Trailing Stop' or 'security()' functions (although using a security function doesn`t mean that the script repaints) and all signals are confirmed, therefore the script doesn`t repaint in alert mode and is accurate in backtest mode.

Apart from the previous indicators, some more and other functions have been added for Stop-Loss, re-entry and leverage.

It uses 8 indicators, (many of you already know what they are, but in case there is someone new), these are the following:

1. Jurik Moving Average

It's a moving average created by Mark Jurik for professionals which eliminates the 'lag' or delay of the signal. It's better than other moving averages like EMA , DEMA , AMA or T3.

There are two ways to decrease noise using JMA . Increasing the 'LENGTH' parameter will cause JMA to move more slowly and therefore reduce noise at the expense of adding 'lag'

The 'JMA LENGTH', 'PHASE' and 'POWER' parameters offer a way to select the optimal balance between 'lag' and over boost.

Green: Bullish , Red: Bearish .

2. Range filter

Created by Donovan Wall, its function is to filter or eliminate noise and to better determine the price trend in the short term.

First, a uniform average price range 'SAMPLING PERIOD' is calculated for the filter base and multiplied by a specific quantity 'RANGE MULTIPLIER'.

The filter is then calculated by adjusting price movements that do not exceed the specified range.

Finally, the target ranges are plotted to show the prices that will trigger the filter movement.

Green: Bullish , Red: Bearish .

3. Average Directional Index ( ADX Classic) and ( ADX Masanakamura)

It's an indicator designed by Welles Wilder to measure the strength and direction of the market trend. The price movement is strong when the ADX has a positive slope and is above a certain minimum level 'ADX THRESHOLD' and for a given period 'ADX LENGTH'.

The green color of the bars indicates that the trend is bullish and that the ADX is above the level established by the threshold.

The red color of the bars indicates that the trend is down and that the ADX is above the threshold level.

The orange color of the bars indicates that the price is not strong and will surely lateralize.

You can choose between the classic option and the one created by a certain 'Masanakamura'. The main difference between the two is that in the first it uses RMA () and in the second SMA () in its calculation.

4. Parabolic SAR

This indicator, also created by Welles Wilder, places points that help define a trend. The Parabolic SAR can follow the price above or below, the peculiarity that it offers is that when the price touches the indicator, it jumps to the other side of the price (if the Parabolic SAR was below the price it jumps up and vice versa) to a distance predetermined by the indicator. At this time the indicator continues to follow the price, reducing the distance with each candle until it is finally touched again by the price and the process starts again. This procedure explains the name of the indicator: the Parabolic SAR follows the price generating a characteristic parabolic shape, when the price touches it, stops and turns ( SAR is the acronym for 'stop and reverse'), giving rise to a new cycle. When the points are below the price, the trend is up, while the points above the price indicate a downward trend.

5. RSI with Volume

This indicator was created by LazyBear from the popular RSI .

The RSI is an oscillator-type indicator used in technical analysis and also created by Welles Wilder that shows the strength of the price by comparing individual movements up or down in successive closing prices.

LazyBear added a volume parameter that makes it more accurate to the market movement.

A good way to use RSI is by considering the 50 'RSI CENTER LINE' centerline. When the oscillator is above, the trend is bullish and when it is below, the trend is bearish .

6. Moving Average Convergence Divergence ( MACD ) and ( MAC-Z )

It was created by Gerald Appel. Subsequently, the histogram was added to anticipate the crossing of MA. Broadly speaking, we can say that the MACD is an oscillator consisting of two moving averages that rotate around the zero line. The MACD line is the difference between a short moving average 'MACD FAST MA LENGTH' and a long moving average 'MACD SLOW MA LENGTH'. It's an indicator that allows us to have a reference on the trend of the asset on which it is operating, thus generating market entry and exit signals.

We can talk about a bull market when the MACD histogram is above the zero line, along with the signal line, while we are talking about a bear market when the MACD histogram is below the zero line.

There is the option of using the MAC-Z indicator created by LazyBear, which according to its author is more effective, by using the parameter VWAP ( volume weighted average price ) 'Z-VWAP LENGTH' together with a standard deviation 'STDEV LENGTH' in its calculation.

7. Volume Condition

Volume indicates the number of participants in this war between bulls and bears, the more volume the more likely the price will move in favor of the trend. A low trading volume indicates a lower number of participants and interest in the instrument in question. Low volumes may reveal weakness behind a price movement.

With this condition, those signals whose volume is less than the volume SMA for a period 'SMA VOLUME LENGTH' multiplied by a factor 'VOLUME FACTOR' are filtered. In addition, it determines the leverage used, the more volume , the more participants, the more probability that the price will move in our favor, that is, we can use more leverage. The leverage in this script is determined by how many times the volume is above the SMA line.

The maximum leverage is 8.

8. Bollinger Bands

This indicator was created by John Bollinger and consists of three bands that are drawn superimposed on the price evolution graph.

The central band is a moving average, normally a simple moving average calculated with 20 periods is used. ('BB LENGTH' Number of periods of the moving average)

The upper band is calculated by adding the value of the simple moving average X times the standard deviation of the moving average. ('BB MULTIPLIER' Number of times the standard deviation of the moving average)

The lower band is calculated by subtracting the simple moving average X times the standard deviation of the moving average.

the band between the upper and lower bands contains, statistically, almost 90% of the possible price variations, which means that any movement of the price outside the bands has special relevance.

In practical terms, Bollinger bands behave as if they were an elastic band so that, if the price touches them, it has a high probability of bouncing.

Sometimes, after the entry order is filled, the price is returned to the opposite side. If price touch the Bollinger band in the same previous conditions, another order is filled in the same direction of the position to improve the average entry price, (% MINIMUM BETTER PRICE ': Minimum price for the re-entry to be executed and that is better than the price of the previous position in a given %) in this way we give the trade a chance that the Take Profit is executed before. The downside is that the position is doubled in size. 'ACTIVATE DIVIDE TP': Divide the size of the TP in half. More probability of the trade closing but less profit.

█ STOP LOSS and RISK MANAGEMENT.

A good risk management is what can make your equity go up or be liquidated.

The % risk is the percentage of our capital that we are willing to lose by operation. This is recommended to be between 1-5%.

% Risk: (% Stop Loss x % Equity per trade x Leverage) / 100

First the strategy is calculated with Stop Loss, then the risk per operation is determined and from there, the amount per operation is calculated and not vice versa.

In this script you can use a normal Stop Loss or one according to the ATR. Also activate the option to trigger it earlier if the risk percentage is reached. '% RISK ALLOWED'

'STOP LOSS CONFIRMED': The Stop Loss is only activated if the closing of the previous bar is in the loss limit condition. It's useful to prevent the SL from triggering when they do a ‘pump’ to sweep Stops and then return the price to the previous state.

█ BACKTEST

The objective of the Backtest is to evaluate the effectiveness of our strategy. A good Backtest is determined by some parameters such as:

- RECOVERY FACTOR: It consists of dividing the 'net profit' by the 'drawdown’. An excellent trading system has a recovery factor of 10 or more; that is, it generates 10 times more net profit than drawdown.

- PROFIT FACTOR: The ‘Profit Factor’ is another popular measure of system performance. It's as simple as dividing what win trades earn by what loser trades lose. If the strategy is profitable then by definition the 'Profit Factor' is going to be greater than 1. Strategies that are not profitable produce profit factors less than one. A good system has a profit factor of 2 or more. The good thing about the ‘Profit Factor’ is that it tells us what we are going to earn for each dollar we lose. A profit factor of 2.5 tells us that for every dollar we lose operating we will earn 2.5.

- SHARPE: (Return system - Return without risk) / Deviation of returns.

When the variations of gains and losses are very high, the deviation is very high and that leads to a very poor ‘Sharpe’ ratio. If the operations are very close to the average (little deviation) the result is a fairly high 'Sharpe' ratio. If a strategy has a 'Sharpe' ratio greater than 1 it is a good strategy. If it has a 'Sharpe' ratio greater than 2, it is excellent. If it has a ‘Sharpe’ ratio less than 1 then we don't know if it is good or bad, we have to look at other parameters.

- MATHEMATICAL EXPECTATION: (% winning trades X average profit) + (% losing trades X average loss).

To earn money with a Trading system, it is not necessary to win all the operations, what is really important is the final result of the operation. A Trading system has to have positive mathematical expectation as is the case with this script: ME = (0.87 x 30.74$) - (0.13 x 56.16$) = (26.74 - 7.30) = 19.44$ > 0

The game of roulette, for example, has negative mathematical expectation for the player, it can have positive winning streaks, but in the long term, if you continue playing you will end up losing, and casinos know this very well.

PARAMETERS

'BACKTEST DAYS': Number of days back of historical data for the calculation of the Backtest.

'ENTRY TYPE': For '% EQUITY' if you have $ 10,000 of capital and select 7.5%, for example, your entry would be $ 750 without leverage. If you select CONTRACTS for the 'BTCUSDT' pair, for example, it would be the amount in 'Bitcoins' and if you select 'CASH' it would be the amount in $ dollars.

'QUANTITY (LEVERAGE 1X)': The amount for an entry with X1 leverage according to the previous section.

'MAXIMUM LEVERAGE': It's the maximum allowed multiplier of the quantity entered in the previous section according to the volume condition.

The settings are for Bitcoin at Binance Futures (BTC: USDTPERP) in 15 minutes.

For other pairs and other timeframes, the settings have to be adjusted again. And within a month, the settings will be different because we all know the market and the trend are changing.

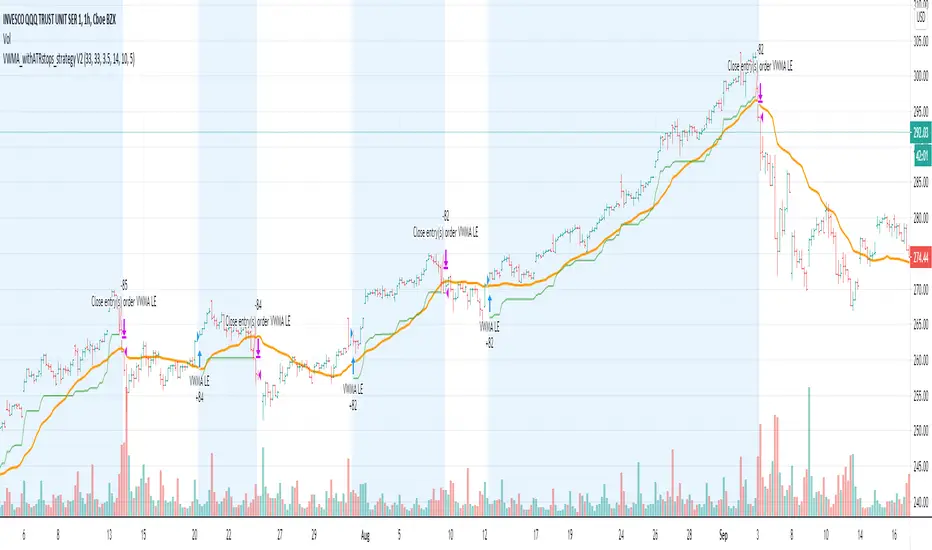

VWMA_withATRstops_strategyThis strategy follows the trend when price is above VWMA indicator. I have modified entry and exit rules to get most out of it.

Instead of entering LONG when price crosses above VWMA, I have used RSI(14) of VWMA . that way it skips the false signals. (some extent)

ENTRY

========

1. VWMA setting is 33

2. When RSIofVwma is above 30 enter Long ( and also checks if price already broke the ATR Stop above line )

Stop Loss and Exits

==================

1. Exit is when price breaks the ATR stop loss

2. ATR setting is set as same VWMA Length and multiplier is 3.5

3. STOP Loss that I mentioned in the settings is being used to calculate the how many units can be purchased based on risk of capital value.

Note: There is NO hard stop loss. having above ATR stop loss works as Trailing stop loss

Warning

=======

For the educational purposes only

Fibonacci Bollinger Bands Strategy [QuantNomad]This strategy is modified Stanard Bollinger Bands Strategy. Instead of using standard deviation, I use a metric of how big is the range for the last X bars. Also, I’m using Fibonacci levels as multipliers for BB.

In this strategy you have a choice of 3 different Trailing Stop Loss types:

Standard % – standard percent based TSL

Fibonacci Level – close your position on another Fibonacci level or basis line of BB.

Parabolic SAR – Parabolic SAR adapted as trailing stop loss.

For Standard % and Parabolic SAR, you can use the “TSL Offset” parameter to set an initial offset for trailing stop loss.

Parameters

BB Length – Bolinger Bands Length

Fib Entry Level – Entry BB Multiplier level. Can be one of Fibonacci levels: 0.236, 0.382, 0.5, 0.618, 0.786, 1.000

Trailing SL Type – Type of Trailing Stop Loss used to close positions. Can be one of 3 types: “Standard %”, “Fibonacci Level”, “Parabolic SAR”

TSL Offset (%) – Initial offset for TSL. Applicable to “Standard %” and “Parabolic SAR”

TSL Fib Level – Fibonacci level used for “Fibonacci level” type of TSL

TSL PSAR Start / Increment / Maximum – parameters for PSAR type of TSL.

Strategy side – you can choose the side of the strategy. You can require strategy to go only Long, Short to Both sides.

From/To Day/Month/Year – you can use these parameters to set backtesting range to check the performance of your strategy on a specific range

It's a pro indicator, you can have access to it for a small fee. Link to my PRO indicators you can find in my signature.

Disclaimer

Please remember that past performance may not be indicative of future results.

Due to various factors, including changing market conditions, the strategy may no longer perform as good as in historical backtesting.

This post and the script don’t provide any financial advice.

Trend spider glueThis script works on all market types.

This script will show you when to long, short, exit (stop loss) and Take profit.

Signals take into account various elements such as momentum, volume , moving averages and long term trend analysis. Stop loss function is included to show you when a signal is invalidated.

Use this strategy strictly, patiently and with discipline to prevent unneeded losses, this will result in long term consistent profits.

This script has been set to work best on the intraday time frames, however it also works on the longer timeframes. Use the settings tab to dilute the indicators to ur own market.

Lastly, this indicator will not give signals if the market is not trending.

PM me here to get a free trial for the indicator !

HAPPY TRADING <3

Version 2 will be coming soon which will integerate more elements to allow for more accurate signals and faster stop losses !

disclaimer: although this indicator is taking many elements into account and is highly accurate the market is never certain, we are not responsible for any losses the script may result in as we are not financial advisors.

specific breakout FiFTOStrategy Description: 10:14 Breakout Only

Overview This is a time-based intraday trading strategy designed to capture momentum bursts that occur specifically after the 10:14 AM candle closes. It operates on the logic that if price breaks the high of this specific candle within a short window, a trend continuation is likely.

Core Logic & Rules

The Setup Candle (10:14 AM)

The strategy waits specifically for the minute candle at 10:14 to complete.

Once this candle closes, the strategy records its High price.

Defining the Entry Level

It calculates a trigger price by taking the 10:14 High and adding a user-defined Buffer (e.g., +1 point).

Formula: Entry Level = 10:14 High + Buffer

The "Active Window" (Expiry)

The trade setup does not remain open all day. It has a strict time limit.

By default, the setup is valid from 10:15 to 10:20.

If the price does not break the Entry Level by the expiry time (default 10:20), the setup is cancelled and no trade is taken for the day.

Entry Trigger

If a candle closes above the Entry Level while the window is open, a Long (Buy) position is opened immediately.

Exits (Risk Management)

Stop Loss: A fixed number of points below the entry price.

Target: A fixed number of points above the entry price.

Visual & Automation Features

Visual Boxes: Upon entry, the strategy draws a "Long Position" style visual on the chart. A green box highlights the profit zone, and a red box highlights the loss zone. These boxes extend automatically until the trade closes.

JSON Alerts: The strategy is pre-configured to send data-rich alerts for automation (e.g., Telegram bots).

Entry Alert: Includes Symbol, Entry Price, SL, and TP.

Exit Alerts: Specific messages for "Target Hit" or "SL Hit".

Summary of User Inputs

Entry Buffer: Extra points added to the high to filter false breaks.

Fixed Stop Loss: Risk per trade in points.

Fixed Target: Reward per trade in points.

Expiry Minute: The minute (10:xx) at which the setup becomes invalid if not triggered.

Third eye • StrategyThird eye • Strategy – User Guide

1. Idea & Concept

Third eye • Strategy combines three things into one system:

Ichimoku Cloud – to define market regime and support/resistance.

Moving Average (trend filter) – to trade only in the dominant direction.

CCI (Commodity Channel Index) – to generate precise entry signals on momentum breakouts.

The script is a strategy, not an indicator: it can backtest entries, exits, SL, TP and BreakEven logic automatically.

2. Indicators Used

2.1 Ichimoku

Standard Ichimoku settings (by default 9/26/52/26) are used:

Conversion Line (Tenkan-sen)

Base Line (Kijun-sen)

Leading Span A & B (Kumo Cloud)

Lagging Span is calculated but hidden from the chart (for visual simplicity).

From the cloud we derive:

kumoTop – top of the cloud under current price.

kumoBottom – bottom of the cloud under current price.

Flags:

is_above_kumo – price above the cloud.

is_below_kumo – price below the cloud.

is_in_kumo – price inside the cloud.

These conditions are used as trend / regime filters and for stop-loss & trailing stops.

2.2 Moving Average

You can optionally display and use a trend MA:

Types: SMA, EMA, DEMA, WMA

Length: configurable (default 200)

Source: default close

Filter idea:

If MA Direction Filter is ON:

When Close > MA → strategy allows only Long signals.

When Close < MA → strategy allows only Short signals.